October 18, 2025 | Reading time: ~45 min

In October 2025, the economic conflict between China and the United States entered a new, exceptionally dramatic phase. Beijing introduced unprecedented restrictions on the export of critical raw materials, directly targeting the American defense sector. Washington responded with the threat of 100% tariffs on all goods from China. These exchanges—concerning such exotic materials as dysprosium, germanium, and antimony—sent shockwaves through financial markets and raised a crucial question: are we witnessing the irreversible separation (decoupling) of the world’s two largest economies?

Tensions have never been higher. Stock market valuations plummeted, with two trillion dollars of corporate value in the US evaporating in a single day. Simultaneously, the prices of some metals skyrocketed (antimony trichloride has risen by 228% since the beginning of the year!), and the shares of mining companies outside of China exploded. Strategists on both sides of the Pacific are speaking bluntly—the stakes are technological superiority and national security, and critical raw materials have become a geopolitical weapon. As a result, what was recently an abstract concept from think-tank analyses—”decoupling,” the separation of US and Chinese supply chains—is now taking on a very real form.

In this comprehensive article, we analyze the evolution of this conflict: from the buildup of Chinese dominance in raw materials, through the initial trade clashes and sanctions, to the current escalation. We explain what critical raw materials are and why their availability is crucial for modern armies and economies. We examine the potential geopolitical and economic consequences—from the production lines of F-35 fighter jets to the prices of electric cars. We also describe the United States’ strategy to reduce its dependence on China: from investing in its own mines, through alliances with other countries, to recycling and creating strategic reserves. Finally, we consider whether a full economic separation of the West and China is actually feasible, what development scenarios are in play, and what the coming years mean for Europe (including Poland), business, and investors.

I. INTRODUCTION

Within just a few days in October 2025, US-China trade relations eroded dramatically. On October 9, Beijing announced a ban on the export of several rare earth elements with military applications to the United States, including dysprosium, terbium, and yttrium. This was the first time China’s raw material restrictions had been so directly aimed at American defense. In response, the next day, President Donald Trump announced retaliatory 100% tariffs on all imports from China, effective November 1. This tit-for-tat exchange—direct and escalatory—raised the burning question: are we on the verge of a complete economic “divorce” between the two powers?

Article’s Thesis

Are we witnessing the irreversible separation of the world’s largest economies? Such a scenario, termed decoupling, seemed extreme just a few years ago. Today, however, after years of mounting tensions and sanctions, it is becoming increasingly realistic. China and the US are systematically reducing their technological and raw material interconnections, citing national security. This article posits that October 2025 may go down in history as a turning point—a moment when the decoupling process significantly accelerated. We will attempt to assess whether this separation is indeed inevitable and permanent, or if there is still a path toward de-escalation and managed interdependence.

Context: Why is this conflict happening now?

As recently as the early 2010s, US-China economic relations were described as symbiotic: China became the “world’s factory,” supplying America with cheap goods, while American companies and consumers benefited from low production costs. However, beneath this interdependence, tensions were growing. Washington has long been concerned about its dependence on Chinese supplies of key components and materials—from electronics to strategic minerals. Beijing, in turn, views American technological sanctions (e.g., restrictions on advanced chips) as an attempt to halt its development.

Critical raw materials have become a focal point of this conflict for several reasons:

- China’s Monopolistic Position – For years, Beijing has built up its dominance in the extraction and processing of strategic metals. It currently controls, among other things, about 70% of the world’s rare earth element mining and a staggering 92% of their processing, nearly 98% of global gallium production, and about 60-80% of germanium production. This concentration raises fears that China could use the “raw materials tap” as a tool of pressure.

- Crucial Military-Technological Importance – These materials are essential for producing advanced weaponry (stealth fighters, missiles, communication systems) and future technologies (electric cars, renewable energy, semiconductors). Shortages could paralyze the defense industry and undermine economic competitiveness.

- Escalation of Actions by Both Sides – Starting with the 2018 tariff war, through US sanctions on Chinese companies (Huawei, SMIC) and technology export controls, to China’s counter-moves (export restrictions on metals like germanium and graphite). Each year brought new restrictions that, step by step, limited free trade in strategic sectors.

- Current Events – Right now, another series of moves is unfolding: a Chinese embargo on raw materials for the US military and an aggressive US response in the form of tariffs. Both countries are thus approaching a red line, beyond which a permanent rupture of global supply chains may occur.

In this article, we will examine the genesis and course of these tensions to understand their significance and possible consequences. In Section II, we will go back to the beginning—how China gained its raw material dominance and when the conflict began. Section III will explain what critical raw materials are and why controlling them provides a strategic advantage. In Section IV, we will assess the geopolitical and economic effects—is the US facing a national security crisis? How will sectors from semiconductors to automotive suffer? Section V will describe America’s defensive strategy: building its own supply sources, collaborating with allies, innovating, and stockpiling reserves. In Section VI, we will consider whether a full decoupling is realistic—we will present arguments for and against, as well as possible scenarios (from managed coexistence, through a total split, to a potential reset). Then, in Section VII, we will discuss what these global struggles mean for Europe and Poland—both in terms of risks (e.g., for the automotive industry) and opportunities (e.g., new investments in the region). Finally, Section VIII will summarize the most important conclusions and future prospects.

💡 KEY TAKEAWAY

Critical raw materials have become a key front in the US-China rivalry. China controls the lion’s share of the world’s production of these materials, giving it a potential “economic weapon.” October 2025 brought an escalation: a Chinese embargo on metals for the US and American super-tariffs. This could be a turning point in the process of decoupling—the gradual unraveling of the economic ties between the two superpowers.

II. HISTORY OF TENSIONS – FROM INTERDEPENDENCE TO CONFLICT

To understand the current situation, we must trace the evolution of US-China economic relations in the context of strategic raw materials. Over the last few decades, they have come a long way: from apparent harmony and mutually beneficial cooperation, through growing rivalry, to open trade conflict. Below, we present three key stages of this history.

2.1 The Buildup of China’s Raw Material Dominance (1980s–2010)

China’s current advantage in the critical raw materials sector is no accident—it is the result of a long-term strategy. As early as the 1980s and 1990s, Chinese leaders identified rare earth metals and other strategic minerals as an “ace up their sleeve.” It was Deng Xiaoping who famously said: “The Middle East has oil; China has rare earths.” Beijing consistently put this idea into practice, investing in the development of domestic extraction and processing of key raw materials.

Several factors allowed China to build a near-monopolistic position:

- State Policy and Financial Support – The strategic metals sector was given priority status. The government supported domestic companies through subsidies, tax breaks, and control over energy prices. Investments were made in refining and separation technologies, even if they were initially unprofitable.

- Looser Environmental Regulations – The processing of many raw materials (e.g., rare earth elements or graphite) is dirty and toxic. Western countries, having tightened environmental standards, effectively withdrew from this activity. China, on the other hand, tolerated higher environmental costs for years. The result? Production moved to where it was cheaper and “easier,” which was China.

- Scale and Cheap Labor – Chinese mines and smelters could produce on a massive scale using cheap labor. This dramatically lowered the prices of many metals. Competitors in the West went bankrupt, unable to compete with Chinese dumping prices.

- Acquisition of Foreign Assets – Chinese companies (often state-backed) acquired deposits and raw material companies abroad to secure supplies. An example is the high-profile attempt by the Chinese to acquire the Australian company Lynas (operating in Malaysia)—the only major rare earth processor outside of China. Although a full buyout did not occur thanks to the intervention of the Australian and Japanese governments, such attempts signaled China’s ambitions to control the global supply chain.

By the end of the 2000s, the West “woke up” to a new reality: critical raw materials, once also produced in the US, EU, or Japan, now overwhelmingly came from China. For example, in 2009, China accounted for ~97% of the world’s production of rare earth elements. The American Mountain Pass mine in California—once the main Western supplier of rare earths—was closed in 2002 due to bankruptcy and environmental issues. The whole world became dependent on Chinese supplies because it was cheaper and more convenient.

The only rare earth element mine in the US – Mountain Pass, California (aerial view). It has been operating since the 1960s but suspended mining for over a decade in 2002 due to Chinese competition and environmental restrictions. Until recently, its entire output was sent to China for processing. Only recently, with Pentagon support, has basic metal separation been launched on-site.

The 2010 Lesson: The First “Warning.” China’s dominance did not attract widespread attention until an incident in the fall of 2010. After a Chinese fishing trawler captain was detained by the Japanese (the incident around the disputed Senkaku/Diaoyu islands), China unofficially halted the export of rare earth elements to Japan. Although Beijing never officially confirmed such an embargo, for about two months, Japanese companies could not receive supplies of key metals. For Tokyo—which at the time imported 90% of these raw materials from China—it was a shock. The prices of neodymium and cerium, for example, skyrocketed several times over, and Japanese electronics and automotive manufacturers panicked.

📊 CASE STUDY: China’s 2010 Embargo on Japan

Background: In September 2010, Japan detained a Chinese fishing trawler near a disputed island, sparking a diplomatic crisis.

China’s Action: Although no official declaration was made, Chinese supplies of rare earth elements to Japan were reportedly halted for about 2 months. Chinese authorities used their control over the global market for these metals to exert pressure on Tokyo.

Result: Japanese companies (Toyota, Panasonic, etc.) faced the prospect of production disruptions for advanced components. The prices of some metals jumped by several hundred percent. The crisis was eventually resolved—Japan released the trawler captain—and supplies resumed.

Lessons: Japan realized it could “never again” be so dependent on a single supplier. In the following years, it invested in diversification: it financially supported the development of the Australian Lynas mine (to become independent of China), began recycling used magnets, and reduced its consumption of some elements. Within a decade, Japan’s imports of rare earths from China fell from ~90% to ~60%.

On a broader scale: The incident made the entire world aware that China was willing to “weaponize” its raw material dominance for political purposes. The US and Europe also drew conclusions—serious thought began to be given to securing critical supplies. In 2014, the US, EU, and Japan won a WTO case against China regarding export restrictions, forcing Beijing to lift some export quotas. But the mechanism remained: China had shown it could turn off the tap if it deemed it appropriate.

2.2 The First Phase of Tensions (2018–2023)

Despite the warning signs from 2010, global business continued to benefit from cheap Chinese supplies for the next decade. However, the growing US-China rivalry in trade and technology foreshadowed changes. The first flashpoint was the trade war during Donald Trump’s presidency (first term, 2017–2021). In 2018, the Trump administration imposed punitive tariffs on hundreds of billions of dollars worth of Chinese goods, accusing Beijing of unfair practices (intellectual property theft, industrial subsidies, currency manipulation). China responded with its own tariffs on American products. A period of growing economic mistrust began.

Although the focus at the time was mainly on mass-produced goods (steel, aluminum, consumer products), the issue of technology and critical raw materials was already looming. Key events of this phase include:

- October 2022 – “Chip War”: The US government (now under President Biden) introduced strict export restrictions on semiconductors and the equipment to produce them to China. In practice, China was cut off from the most advanced integrated circuits (e.g., AI chips from Nvidia) and the software and machinery (EUV lithography) necessary for their manufacture. This was a blow to China’s technological ambitions—Washington made it clear that it would not allow Beijing to gain an advantage in key technologies like artificial intelligence or quantum computing. China described this as a “technological blockade.”

- 2023 – The First Chinese Raw Material Counter-Offensives: Beijing began to leverage its advantages in critical raw materials. In July 2023, it announced export controls on gallium and germanium—two niche but important metals for the semiconductor, fiber optics, and energy industries. Exporters had to obtain licenses to ship these raw materials abroad, which created immense uncertainty. Gallium prices surged several times over on the news of these restrictions. Then, in October 2023, China imposed controls on the export of graphite (a material essential for the production of lithium-ion batteries). In both cases, the official justification was “protecting national security” and concern about the use of Chinese raw materials to produce advanced military equipment abroad. In practice, this was a response to the American chip restrictions—Beijing was signaling that if it couldn’t buy chips, it would make it difficult to access the materials needed to make them.

- 2021–2023 – Other Tensions: It’s worth noting that during this period, China also used non-trade retaliatory measures. For example, it restricted investments by American companies in China and launched antitrust investigations against US corporations. On the other hand, the US expanded its blacklists of Chinese companies (adding, for instance, SMIC—China’s largest semiconductor manufacturer—to the list of entities subject to export restrictions). The world began to watch the two economies “slide” towards separation in high-tech areas. However, until 2023, there was no complete severing of ties—restrictions applied to selected sectors and products, while overall trade was still booming (in 2022, US-China trade reached a record $690 billion).

This first phase of tensions revealed the underlying dynamic: the US used its advantage in technology (e.g., chips) as a tool of pressure on China, and China began to use its advantage in raw materials as retaliation. It was only a matter of time before this tug-of-war expanded to a wider range of materials.

2.3 Escalation in 2024–2025

After a relative ceasefire (the “truce” phase of the trade war agreed upon under Trump in January 2020, the so-called Phase One deal), the next escalation occurred in 2024 and gained momentum in 2025. It can be said that during this period, the “spirit of decoupling” clearly began to hang over the actions of both sides. Here are the most important events from this period:

- August 2024 – Antimony Restrictions: China introduced export limits and tightened controls on another raw material—antimony. This semi-metal is crucial, among other things, for the defense industry (more on this in Section III), and China supplies about half of the world’s production. After these restrictions, antimony supplies from China dropped dramatically—by October 2024, exports had fallen by 97% compared to previous months. Prices shot up, and chemical and defense companies in the West began to nervously buy up inventories.

- December 2024 – “Full Ban” on Exports of Selected Minerals to the US: On December 3, 2024, Beijing went all-in, announcing that “in principle, the export of gallium, germanium, antimony, and superhard materials to the United States will not be permitted.” This was retaliation announced a day after Washington again expanded sanctions on the Chinese semiconductor sector. The then-announcement from the Chinese Ministry of Commerce spoke of “protecting national security” and also included tightening controls on graphite exports to the US. In practice, China imposed an embargo on three key raw materials for the US:

- Gallium – used in semiconductor compounds (GaN, GaAs) and optoelectronics.

- Germanium – used in fiber optics, night vision, and solar panels.

- Antimony – needed for ammunition, military electronics, and batteries.

This step was groundbreaking: for the first time, China directly targeted the US by cutting off the supply of strategic raw materials. Although gallium and germanium exports had already slowed significantly due to the July licensing requirements (customs data showed that virtually nothing had been sent to the US since August 2023), the December ban legally sealed the deal. Beijing sent a signal: “since you are strangling our chip industry, we will choke your access to critical minerals.” This was, in effect, the “weaponization” of raw material exports, as directly labeled by Western commentators (e.g., the CEO of Perpetua said that “China has weaponized mineral access”).

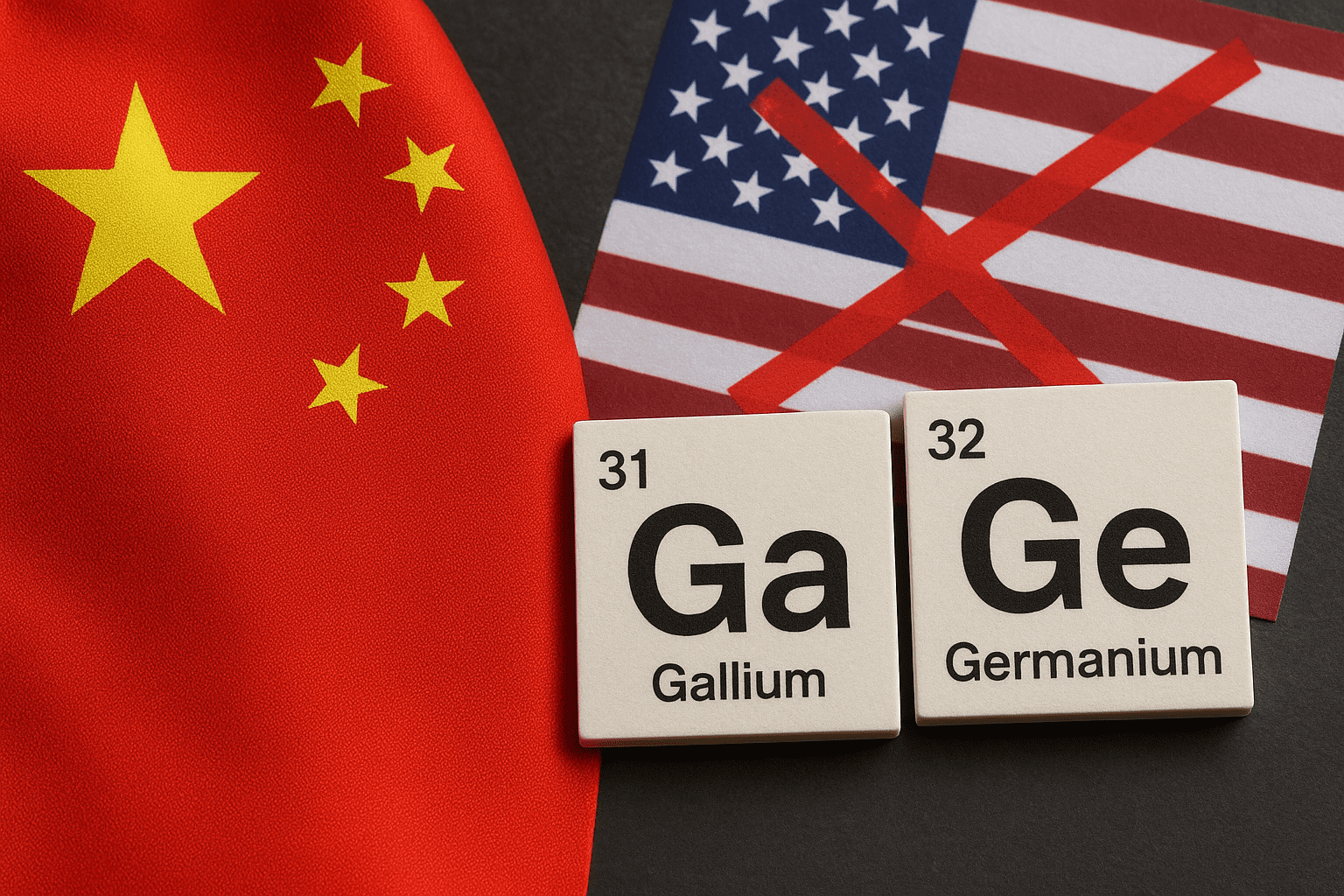

The symbols for the elements Ga (gallium) and Ge (germanium) on the periodic table, against the backdrop of the US and Chinese flags. These two lesser-known metals have become the subject of a fierce struggle: China first introduced export licenses for them (July 2023), and then in December 2024, completely banned their sale to the US. Both are essential for the production of advanced semiconductors, making them strategic raw materials in an era of technological rivalry.

- January 2025 – Change in US Administration and Continuation of a Hardline Stance: In January 2025, Donald Trump returned to power (re-elected as president in the 2024 election). During his campaign, he had promised a tougher approach to China. After taking office, he quickly moved from words to deeds. In April 2025, he announced so-called “reciprocal tariffs”—a drastic increase in import duties on products from countries that he believed were “cheating on trade.” This was aimed primarily at China, but also at countries that maintain high tariffs on American goods. In practice, the US raised tariffs on Chinese imports to an average of 45% (from the 25% in place since the previous trade war). Trump argued that since China restricts raw material exports and subsidizes its own exports, the US must defend itself with equivalent fees. In response, Beijing tore up the previous trade truce: it also raised retaliatory tariffs (though the scale is asymmetric—China imports less from the US). Importantly, in the background of all this, the United States managed to persuade its allies to cooperate more closely: by spring 2025, the European Union and Japan had essentially aligned with American restrictions on technology exports to China (albeit with a delay). Washington applied pressure, for instance, by threatening tariffs on European products if they served as a “backdoor” for Chinese semiconductor imports. This shows that the seeds of economic blocs were being sown—the US and its partners versus China and its friendly states.

- April 2025 – Expansion of Chinese Controls to 7 Rare Earth Elements: Chinese authorities, reacting to another wave of Trump’s tariffs, decided to go further with raw material restrictions. On April 4, 2025, it was announced that the export of seven rare earth elements (samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium) and magnets containing them would require special permits. Significantly, these were mainly medium and heavy rare earth elements—the rarer and more critical ones (more on them in Section III). Controls were also introduced on the export of technologies related to rare earth refining and magnet production. It was not yet a formal ban—more of a licensing mechanism—but it effectively had the same result as with gallium and germanium: global customers began to fear supply disruptions.

It’s worth noting that the Chinese regulation went even further: it covered not only the export of the raw material itself but also situations where foreign companies wanted to sell products containing Chinese rare earths or produced using Chinese technology. This was a mirror image of the American FDPR (Foreign Direct Product Rule), which the US uses to restrict chip exports to China (a ban on selling anything produced using American tools/technology). In other words: China decided that since the US is globally blocking technology access to China, China will globally block material access to technology. - October 2025 – The October Escalation (Events Described in the Introduction): The situation culminates at the moment described in the introduction. China expands its “blacklist” of raw materials to 12 of the 17 rare earth elements—adding another 5 in October (holmium, erbium, thulium, europium, and ytterbium). This means that almost all key elements in this group are under control. Furthermore, it was officially announced that no rare earth material could go to foreign military customers. In practice, as the Chinese Ministry of Commerce explained, “as long as these elements are used for civilian purposes, exports will be approved”—suggesting that any connection to the defense industry would result in a license denial. In other words: the US will no longer get Chinese raw materials needed to build missiles, planes, or radars. This is an almost unprecedented step. Expert Gracelin Baskaran from CSIS assessed that “this is an unprecedented move—never before have mineral restrictions gone this far and so deliberately targeted our defense industry,” adding that “China is backing us into a corner on national security by weaponizing rare earth exports.”

Trump reacted almost immediately, announcing on October 10 that 100% tariffs on all imports from China would take effect on November 1. This meant effectively cutting off Chinese goods from the American market (because such a tariff level makes them unprofitable). Financial markets panicked, after which… Trump softened his tone, tweeting (or rather, “truthing” on Truth Social) a few days later: “Don’t worry about China, everything will be fine! The USA wants to help China, not harm it!!!” It turned out that frantic negotiations had taken place behind the scenes—Treasury Secretary Scott Bessent held a series of calls with his Chinese counterpart over the weekend, which helped to calm the situation somewhat. “We held intensive consultations, which helped to de-escalate the situation,” Bessent admitted. Nevertheless, formally, neither side has backed down from its decisions—the tariffs were set to take effect, as were the Chinese restrictions (though Beijing postponed their full implementation until December, likely to allow time for talks at the planned Trump-Xi summit).

US President Donald Trump and PRC Chairman Xi Jinping plan to meet at the end of 2025 at the APEC summit in South Korea. This will be their first face-to-face conversation since the escalation of sanctions and tariffs. Many observers hope it will halt the spiral of the raw material conflict, although for now, both sides have taken firm positions.

To summarize the historical retrospective: over a dozen years, US-China relations have moved from deep interdependence to open rivalry and hybrid economic warfare. Critical raw materials—once a niche topic for geologists—have become a matter of the highest state importance. China consciously built an advantage in this area and is now using it without hesitation. The United States, dependent on these supplies, is trying to respond with trade pressure and mobilization of allies. Each subsequent move brings both sides closer to decoupling, although channels of dialogue still exist (like the upcoming Trump-Xi summit). Section II showed how we got here. In the next part (III), we will explain why these specific raw materials—rare earth elements, gallium, germanium, antimony, cobalt, and others—are so strategically important.

III. CRITICAL RAW MATERIALS – WHAT’S AT STAKE?

In the previous section, we described the conflict over critical raw materials in geopolitical terms. Now, let’s take a closer look at these materials themselves: what are they, what are their applications, and why does a lack of access to them cause such great concern? The term “critical raw materials” is not accidental—these are materials essential for modern technologies and, at the same time, subject to supply risks (because they come mainly from one country or are difficult to substitute). In this section, we will discuss four key groups:

- Rare Earth Elements (REEs) – the heart of numerous high-tech systems, from electric motors to missile guidance.

- Gallium and Germanium – niche metals with a major role in electronics and photonics.

- Antimony – a semi-metal crucial for the defense and chemical industries.

- Other raw materials – such as cobalt, lithium, nickel, graphite, tungsten, tantalum – also important in the context of technological security.

3.1 Rare Earth Elements (REEs)

Definition and Classification: The rare earth elements group includes 17 metallic chemical elements—scandium, yttrium, and the 15 lanthanides (from lanthanum to lutetium). The name is somewhat misleading: some of them are not rare in the Earth’s crust (e.g., cerium is more common than lead), but they rarely occur in a form suitable for easy extraction. More importantly, their separation and purification is a technologically very complex process. They are divided into two subgroups:

- Light Rare Earth Elements (LREEs) – with lower atomic numbers (57–63: lanthanum, cerium, praseodymium, neodymium, promethium, samarium, europium). They are more common in nature and usually appear together.

- Heavy Rare Earth Elements (HREEs) – with higher atomic numbers (64–71: gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium + yttrium, atomic number 39, which is chemically classified with HREEs). They are much rarer in deposits and more difficult to isolate. They also often have unique properties, making their technological importance disproportionately large.

Key Difference: “light” REEs can be found in a few places in the world outside of China (e.g., in the US, Australia), whereas “heavy” REEs, until recently, came almost exclusively from China. For example, until 2023, China had a nearly 99% share in the global processing of heavy rare earth elements. For light REEs, this monopoly was smaller (there are producers in Australia, the US, and Myanmar), but China’s dominance is still enormous.

Applications: What makes these elements so important? Their unique physicochemical properties. Neodymium, praseodymium, dysprosium, and terbium have strong magnetic properties—when added to alloys, they create the world’s most powerful permanent magnets (NdFeB). Yttrium, europium, and gadolinium have special luminescent and nuclear properties. Erbium, holmium, and thulium, in turn, exhibit interesting optical and magnetic properties at low temperatures. These exotic features translate into a wide range of applications, often in critical, sensitive components:

- Neodymium Magnets (Nd-Fe-B with Tb, Dy additives): This was a true technological “game-changer” of the 1980s—neodymium magnets are several times stronger than traditional (ferrite) ones. They revolutionized electric motors and generators. In a military context:

- They are used in the flight control and propulsion systems of combat aircraft. An F-35 Lightning II fighter jet contains about 920 pounds (417 kg) of rare earth elements, mainly in magnets in the engines, control surface servomechanisms, and radar systems.

- A Virginia-class submarine requires about 2.3 tons (9,200 pounds) of these elements for its propulsion and sonar systems. Without them, modern propulsion (quiet, with variable orientation) would be impossible.

- Tomahawk cruise missiles – magnets in the guidance and flight control systems.

- Predator/Reaper drones – their electric motors (propeller drive) and sensors also use NdFeB magnets, which provide high power with small size and weight, which is crucial in unmanned aerial vehicles.

- Defense and Communication Systems: Rare earth elements are part of high-performance microwave amplifiers and radar modules (e.g., in gallium nitride doped with lanthanides), as well as in lasers and electronic warfare systems. Yttrium and europium are used in the phosphors of screens and night vision displays. Gadolinium is used in neutron sensors (e.g., for detecting fissile materials).

- JDAM Guided Bombs: Although these are simple conversion kits for turning conventional gravity bombs into smart ones, they contain miniature motors, sensors, and electronics where components with rare earth additives may be soldered (e.g., in motion sensors).

- Civilian Applications: The list is equally impressive:

- Wind Turbines – The generator of a turbine (especially modern direct-drive turbines) requires strong magnets with neodymium and dysprosium to efficiently convert the slow rotation of the blades into electrical energy. Each large turbine (5–10 MW) can contain several hundred kilograms of Nd and Dy.

- Electric and Hybrid Cars – The traction motors of most EV models are based on NdFeB magnets (e.g., used in the Tesla Model 3 motors). The pumps and servomechanisms in these cars also use small magnets. A lack of these elements would mean larger, heavier, and less efficient motors (e.g., induction motors without magnets, like in some older Teslas, which have a worse power-to-weight ratio).

- Consumer Electronics – Smartphones (speakers, vibration, camera – mini neodymium magnets), laptops (HDD hard drives have strong neodymium magnets in the heads), headphones, cameras – hundreds of millions of devices contain trace amounts of these elements multiplied by scale.

- MRI and Medical Equipment – While superconducting magnets in MRI scanners do not use REEs (they are based on niobium), other devices like X-ray and PET machines may use lutetium, gadolinium, or europium in radiation detectors.

- Lighting and Screens – Europium and yttrium produce the red color in the phosphors of lamps and LCD/LED monitors; terbium provides the green. Thanks to them, displays have vivid colors.

As you can see, from electric toothbrushes to the F-35, these elements are ubiquitous. However, they are particularly important in weapons and systems critical for defense—and here the problem of dependence on China returns. The United States currently does not have the capability to separate heavy rare earth elements. The only American source (the Mountain Pass mine) produces a concentrate rich in neodymium and praseodymium but poor in heavier elements. Moreover, until recently, 100% of this concentrate was sent to China for further processing! As a result, when it comes to final products (e.g., powdered REE oxides or finished magnets), the US relied almost entirely on imports from China. As recently as 2020–2023, about 70% of the rare earth elements imported by the US came from China (the rest mainly from Estonia, but the refinery there also uses Chinese raw material).

The problematic part is the so-called “separation stage.” Mining the ore is just the beginning—the concentrate contains a mixture of over a dozen elements that are chemically very similar. Separating them requires complex hydrometallurgical processes, hundreds of precipitation cycles in organic solvents, and generates toxic waste (radioactive, because the ores often contain thorium and uranium). For decades, China developed these technologies while the West abandoned them. Until recently, the only heavy REE refinery outside of China (Lynas in Malaysia) faced production limitations and environmental protests. As a result, pure dysprosium or terbium, for example, were not produced at all in the US.

In 2024, the Pentagon admitted in a report that “there is currently no heavy rare earth separation capability in the US; we are building it from scratch.” At the same time, it was stated that every F-35, every submarine, and every JASSM missile is dependent on material supplies from China. This awareness led to a series of actions (described in Section V) to rebuild the domestic rare earth industry. But this is a task that will take years.

In summary: rare earth elements are the “vitamins” of modern technology—without small additions of these metals, many devices would not work at all or would be much less efficient. In military applications, they currently have no real substitutes at a similar level of performance (you can make a motor without NdFeB, but it will be larger and weaker; you can use alternative alloys in some radars, but you lose sensitivity). Therefore, being cut off from rare earths is a strategic nightmare for the US. As an analyst from Benchmark Mineral Intelligence put it: “we are likely entering a period of structural bifurcation—China is localizing its value chain, and the US and its allies are accelerating the construction of their own.” The question is how quickly the West can build this chain.

3.2 Gallium (Ga) and Germanium (Ge)

We now turn to two specific elements that became symbols of Chinese retaliation in 2023: gallium and germanium. These materials are not as “famous” as lithium or uranium, but they are of immense importance in specialized electronics.

What are they?

- Gallium is a metal with atomic number 31, unique in one respect: it melts at a very low temperature—29.76°C. This means it almost melts in your hand (solid at room temperature, but liquid at 30°C). Pure gallium has no wide application, but it is part of semiconductor compounds:

- GaN (gallium nitride) – a material for producing power and microwave transistors, with much better performance at high frequencies and temperatures than silicon.

- GaAs (gallium arsenide) – used since the 1980s in high-speed radio and optoelectronic circuits (lasers, LEDs).

- InGaAs, GaSb, and others – materials for photodetectors, high-efficiency solar cells (multi-junction).

- Germanium (atomic number 32) is a metalloid—something between a metal and a non-metal. It has a structure similar to silicon and was formerly used in the first transistors. Today, its main applications are:

- Ge in fiber optics – germanium is added to the core of glass optical fibers to increase the refractive index and improve transmission parameters.

- Ge in infrared optics – pure germanium is transparent to infrared radiation, so it is used to make lenses and windows for thermal imaging cameras, night vision devices, and IR sights.

- Ge in solar panels – it serves as a substrate (wafer) for multi-junction photovoltaic cells, used mainly in satellites and sometimes in concentrating solar panels (because these cells are very expensive but have high efficiency).

- SiGe (silicon-germanium) – an alloy used in modern RF and digital semiconductor circuits, because adding germanium to silicon improves transistor speed. Used, for example, in chips for 5G networks, signal amplifiers, etc.

- Al-Ga alloy and others – it has some niche uses in special alloys (e.g., in fire sprinklers, there is an alloy with a specific melting point containing gallium and germanium, designed to melt in a fire).

Applications (Summary):

- Advanced Semiconductors:

- GaN is replacing silicon as the material for high-power and high-frequency transistors. It is used in phone chargers (making them smaller and more efficient), DC-DC converters in electric cars (less heat loss), inverters for solar panels, and in radar systems (e.g., AESA radars in modern aircraft).

- GaAs has been the basis for RF modules in smartphones for years (e.g., radio signal power amplifiers) and radar components. Every smartphone has several GaAs chips (in the 4G/5G band).

- InGaAs (indium gallium arsenide) – key in near-infrared detectors (e.g., night vision cameras) and fiber optic photodiodes (telecommunications infrastructure).

- Power Electronics and Renewable Energy: Gallium nitride allows for the creation of very efficient chargers and power supplies (half the size of traditional ones). In photovoltaics, multi-junction cells based on Ga and Ge have record efficiencies (over 40%)—used mainly in space (satellites), but also in specialized ground installations.

- RF and 5G Applications: Many 5G base stations use GaN-based power amplifiers because they can operate at high frequencies (bands above 3 GHz) with lower losses. GaAs/GaN are also used in all types of transmitting devices (from military radars to radio links).

- Optics and Sensors: Germanium is indispensable in thermal imaging—a typical FLIR camera has a germanium lens. The military needs large quantities of germanium for night vision goggles and infrared sights (e.g., for anti-tank launchers, reconnaissance drones, etc.). Smoke detectors and radiation safety devices also use germanium.

- Defense: For military applications, gallium and germanium are quiet but crucial:

- AESA radars in fighter jets (e.g., F-35) – thousands of transmit/receive elements made with GaAs/GaN technology.

- Satellite communication, microwave communication – based on GaAs components.

- Reconnaissance satellites – solar panels based on Ga/Ge provide power.

- Laser weapons, IR jamming systems – semiconductor lasers (e.g., GaAs laser diodes) and Ge detectors.

China’s Dominance: In the case of these two elements, China also plays a leading role:

- Gallium: It is a byproduct of refining bauxite into aluminum. As the world’s largest aluminum producer, China also produces the most gallium. Estimates suggest that 94% to 98% of the global gallium supply comes from China. For years, gallium was a cheap byproduct—China sold it for pennies, which killed off the remaining production in places like Germany. Now, Beijing has turned this into an advantage—when it halted exports, customers had no alternative (in 2022, the US imported 53% of its gallium from China).

- Germanium: The situation here is slightly more dispersed, as germanium is produced during zinc refining and also from lignite coal mining (Germany and Russia also produce it). Nevertheless, China provides about 60-70% of the world’s germanium (data for 2022: ~60%, but after the halt of German production, it may be more). Importantly, China has most of the refining capacity and supplies the most advanced forms (like germanium tetrachloride for fiber optics).

Thus, China’s restrictions on Ga and Ge were like hitting a raw nerve. Western semiconductor and defense companies felt the uncertainty: what if we don’t get these materials? Warehouses began to be filled with emergency stocks. Alternatives were sought: the EU quickly entered into talks with Canada (which has some germanium production) and Kazakhstan (where the Chinese operate zinc smelters). But it’s clear—in the long run, without China, the supply is insufficient and more expensive.

China argued that these restrictions were to protect its security and prevent the use of Chinese materials in foreign defense industries. They also stressed that it was not a ban, but “licenses.” A Ministry of Commerce spokeswoman, He Yongqian, said: “As long as rare earths [here, by implication, also Ga and Ge] are used for civilian purposes, licenses will be issued,” and that the goal was to prevent the proliferation of weapons of mass destruction. This suggests that a company producing chips for cars might get a license, but a manufacturer of military equipment would not. But how to verify the end use of gallium sold to intermediaries? This gives China broad discretion—and that is likely the point.

In summary: gallium and germanium are less “media-friendly” than lithium or neodymium, but their absence would be quickly felt in advanced electronics and communication systems. Both are pillars of 5G connectivity, fiber optics, and infrared sensors. Controlling them allows one to slow down the technological development of an adversary—for example, without gallium, it’s difficult to mass-produce modern base stations, and without germanium, it’s difficult to build large-scale fiber optic networks or advanced IR systems. China understands this and has already used this lever. The West will now intensively seek ways to recycle (e.g., recovering germanium from fiber optic waste) and develop alternative supplies (reactivating old plants?), but this will take time. In the meantime, some agreement on licensing may be reached—because a complete lack of these materials would paralyze not only the US but also certain Chinese industries (with very high raw material prices, even their domestic companies would feel it, so Beijing must strike a balance). This issue is a perfect example of “interdependence”—just as the US cuts China off from chips, China cuts off the raw materials for chips.

3.3 Antimony (Sb)

Another critically important raw material, already mentioned in previous sections, is antimony. It has a long history of use (in ancient Egypt, antimony compounds were used as… eye makeup—kohl). Today, however, we are interested in antimony in modern technology and the military.

Characteristics: Antimony is a lustrous, brittle, silvery-gray semi-metal (semiconductor). Its chemical symbol is Sb (stibium). It does not occur in its native state in nature—it is mainly obtained from the mineral stibnite (antimony sulfide, Sb₂S₃). It is quite toxic on its own. What does it do? When added to metal alloys, it increases their hardness, strength, and wear resistance. Hence its classic application: as an additive to lead.

Key Military Applications:

- Ammunition and Explosives: The lead used in projectiles (e.g., rifle bullets) is hardened with 2-3% antimony, making the bullets less prone to deformation and residue in the barrel. In an alloy with tin, it is used for bullet jackets. Antimony is also a component of primers and explosive-initiating mixtures (e.g., antimony trioxide Sb₂O₃ combined with potassium sulfide was a component of historical gunpowder). Furthermore, stibine (antimony hydride) is a compound used in some pyrotechnics and special explosive mixtures.

- Armor-Piercing Projectiles and Flares: Antimony alloys are used in some kinetic penetrators—for example, antimony is added to tungsten sinters in armor-piercing rounds to improve ballistic properties. In flares and infrared countermeasures, antimony compounds (e.g., antimony hexasulfide) are used to generate intense IR radiation (imitating an engine’s signature).

- Night Vision and Thermal Imaging: Indium antimonide (InSb) is a semiconductor used in the arrays of infrared detectors (mid-wave infrared thermal cameras, ~3-5 micrometers). These types of detectors are found in new-generation night vision goggles, tank observation systems, and the self-guiding heads of infrared-homing missiles (e.g., anti-aircraft missiles). Gallium antimonide (GaSb) and other antimonides are also used in semiconductor lasers emitting in the IR spectrum.

- Nuclear Weapons: While not openly described in literature, historically, antimony (in the form of ¹²⁴Sb) was used in so-called neutron generators (reaction initiators) in the first atomic bombs. Techniques are different now, but antimony is still listed as a strategic material in the context of nuclear weapons (perhaps in shielding, or in certain reactor alloys?). In any case, it is on the lists of critical raw materials for the nuclear sector.

- Military Batteries: Older types of lead-acid batteries (in military vehicles, submarines) contain lead-antimony alloys in the battery plates (antimony improves plate durability). Although modern Ca-Ca batteries have reduced this use, it is still sometimes used in military equipment (easier maintenance during deep discharge).

Civilian Applications:

- Chemical Industry (Flame Retardancy): Antimony trioxide (Sb₂O₃) is a common flame retardant added to plastics, textiles, and paints. When the material ignites, antimony releases halogen gases that suppress the fire. It is used, for example, in electronics casings, cable insulation, and interior furnishings where non-flammability is required.

- Semiconductors and Optical Elements: The aforementioned InSb and GaSb also have civilian uses (thermal imaging cameras for civilian applications, industrial sensors). III-V semiconductors with antimony are also being researched for high-speed transistors.

- Batteries and New-Generation Materials: Work is underway on “flow” batteries and others where antimony can play a role (e.g., liquid antimony anodes). It is also used in some alloys for thermal energy storage.

- Bearing and Sliding Alloys: Tin-antimony-lead alloys (babbitt metal) have long been used for bearing shells. In the energy and automotive industries, this is a key material.

Dependence and Market Dominance:

- China: Possesses about 50-55% of global antimony mining (mainly from the Guangxi and Hunan regions). It also controls a significant portion of refining. Many countries have closed their own mines for environmental and economic reasons (this happened in the US—the last Stibnite mine closed decades ago, and in Canada as well). So, China dictates the supply—as it showed in 2024 by restricting exports and driving up prices.

- Russia/Tajikistan: The second major supplier is the Russian-Tajik deposit in Tajikistan (which holds about 20% of the world’s reserves). However, production there largely goes to China or is controlled by Chinese companies (for example, Talco Gold—a joint venture of the Tajik company TALCO and a Chinese partner).

- Others: Bolivia, Turkey, and Australia produce on a smaller scale. However, no Western country has significant production. The US must import 100% of its needs. In 2018-2021, the main US suppliers were China (approx. 60%), Russia (17%), and the rest from Mexico and India (which likely imported from China anyway).

The Stibnite Gold Project (Perpetua) – America’s Hope: In Idaho, near a former mining site from the World War II era, the company Perpetua Resources is developing the Stibnite gold and antimony mine project. The resources there are estimated at about 6 million ounces of gold and 100 million pounds of antimony (that’s ~45,000 tons of Sb). If it were to start, it could cover ~35-40% of US demand. The Pentagon has deemed it strategic—allocating ~$60 million in grants to support it and lobbying for quick permitting. The US EXIM Bank has declared its readiness to provide up to $1.8 billion in preferential loans for the mine’s construction. This is unprecedented—the US government hasn’t funded mines on this scale for a long time. However, Stibnite is scheduled to start only in 2028 (if it overcomes obstacles—e.g., concerns from the Nez Perce tribe about the mine’s impact on the environment, mainly the salmon population). Until then, the US is condemned to imports, which means vulnerability to pressure—such as Chinese restrictions.

Why is antimony “critical”? Because:

- There are no easy substitutes for its main applications (e.g., selenium or calcium can be used to harden lead, but antimony is more effective; bromine compounds are used as flame retardants, but they are toxic and also controlled).

- It is militarily strategic (you can’t have equally good ammunition bullets without antimony; IR electronics without InSb).

- Its supply is concentrated (China and its satellites).

- The US has no domestic production—complete dependence.

In the context of decoupling, antimony is an example of an “old-school” raw material that has suddenly regained strategic importance. During World War II, it was a key material in the United States (for hardening ammunition, in strategic stockpiles). Later, in times of peace and globalization, it seemed it could be safely imported for pennies from China. Now, history has come full circle: it turns out that in a situation of geopolitical conflict, such a seemingly outdated metal can become the deciding factor. It is enough for China to restrict exports (which it has already done) to force the US into a frantic search for alternatives. Stibnite is that alternative—but it’s a distant prospect. In the meantime, the Pentagon has decided to buy large quantities of antimony for its stockpile (more in Section 5.5)—to survive a potential period of shortage.

3.4 Other Key Raw Materials

To get a full picture of the “raw material theater” in the US-China rivalry, we need to mention a few other materials that are also crucial, although they were not the direct point of contention in October 2025. They also fit into the trend of the US seeking independence from Chinese supplies. Let’s briefly discuss the most important ones:

- Cobalt (Co): A metal used mainly in the chemistry of lithium-ion batteries (in NMC—nickel-manganese-cobalt, and NCA—nickel-cobalt-aluminum cathodes). The addition of cobalt ensures stability and high battery capacity, especially under load (which is crucial, for example, for military electronics). In military applications, cobalt is essential:

- Batteries for portable equipment (radios, GPS systems, night vision devices) – require high energy density and reliability, hence Li-ion with cobalt.

- Unmanned aerial vehicles (drones) – for a reconnaissance drone to operate long and quietly, it needs an efficient battery—usually containing cobalt.

- Energy storage and portable power for soldiers – e.g., the “future soldier” program involves numerous electronic devices that must have powerful batteries.

- Beyond batteries, cobalt is also a component of heat-resistant superalloys (e.g., the turbine blades of jet engines are made of cobalt and nickel alloys—they withstand enormous temperatures).

The problem is that about 70% of the world’s cobalt mining comes from the Democratic Republic of Congo, and the main mines there are controlled by Chinese concerns (China Molybdenum, Huayou Cobalt, etc.). China has monopolized refining—>80% of cobalt is refined in China. Therefore, any shift in relations (or, for example, if China were to strike an exclusive deal with the Congolese government) could cut the West off from cobalt. That is why the US and its allies are trying to develop other sources (projects in Australia, Canada) and recycling (e.g., Redwood Materials in the US recovers cobalt from old batteries). For now, however, the dependence is high—and the Pentagon has already secured funds ($500 million) to build up cobalt reserves.

- Lithium, Nickel, Graphite – The “Big Three” of Li-ion Batteries:

- Lithium: Absolutely key for Li-ion batteries (it cannot be replaced in current chemistry). Global resources are scattered (Chile, Australia, and Argentina dominate mining), but China controls >60% of the capacity for processing lithium into carbonate or hydroxide, the form needed for the battery industry. That’s why, despite the existence of mining in the West, battery factories often have to import lithium chemicals from China. Without lithium, the transformation of electromobility and renewable energy is in question.

- Nickel: A key component of NMC/NCA cathodes in EV batteries (the more nickel, the higher the capacity). The largest mining is in Indonesia and the Philippines, but China is investing heavily there (building huge nickel smelting facilities in Indonesia). Russia (Nornickel) is also a major player. Although Western countries (Australia, Canada) have nickel, China again dominates in refining and producing the chemical forms for batteries. To make matters worse, in 2022, Indonesia imposed a ban on nickel ore exports, which favors Chinese investors building processing plants there—and hurts everyone else (this is analogous to raw material restrictions).

- Graphite: This is the material for the anodes of virtually all current Li-ion batteries. A very pure and properly formed type is required—so-called coated spherical graphite. China controls ~90% of the global production of battery-grade graphite. In 2023, Beijing placed it under export licensing (similar to Ga and Ge). Alternatives? There is work on silicon anodes, but graphite is still indispensable due to its stability. The US plans to build synthetic graphite factories and natural graphite enrichment plants (e.g., the Graphite One project in Alaska—received a $37.5 million grant from the Pentagon). But that’s in the future—currently, virtually every battery in a Tesla or iPhone contains Chinese graphite.

Consequences: The automotive and energy sectors in the West are heavily dependent on these raw materials. If decoupling intensifies, there is a risk of battery shortages, a slowdown in EV production, and an increase in the cost of energy storage (which will hit the climate transition). That’s why both the US and Europe are implementing programs (like the American Inflation Reduction Act, IRA, and the European Critical Raw Materials Act) to stimulate local mining and processing of lithium, nickel, and graphite. But this will take at least several years.

- Tungsten (W) and Tantalum (Ta):

- Tungsten: The metal with the highest melting point among all metals (3422°C). It is irreplaceable in applications requiring hardness and heat resistance. In the military, it is used for the cores of armor-piercing projectiles (mainly tank sub-caliber rounds—a tungsten core penetrates armor kinetically). It is also a component of superalloys in rocket and jet engines (critical elements like nozzles, blades—often tungsten-rhenium alloys). Furthermore, it is used in heavy machinery and radiation shielding (radiological devices). China mines and produces 80-85% of the world’s tungsten. The only significant Western source is a tiny mine in Portugal and Spain; the rest is in Vietnam (which also often goes to China).

- Tantalum: A metal used mainly in tantalum capacitors—which, in turn, are present in almost all electronic devices (especially in military ones, because tantalum capacitors are very reliable and durable). Tantalum in alloys increases strength at high temperatures (it is used, for example, in alloys for aircraft engine components). Due to their huge capacity and small size, tantalum capacitors are in missile control systems, satellites, and radar systems. Unfortunately, most tantalum comes from Africa (DRC, Rwanda), often under difficult conditions (conflict minerals). Australia and Brazil have some, but again—a significant part of the refining and trade is controlled by Chinese entities. In 2020, China was responsible for ~50-60% of the initial refining of tantalum.

A shortage of tungsten or tantalum would hit the defense industry (e.g., it would limit the production of tank ammunition or advanced capacitors). As early as August 2024, China suggested it might restrict tungsten exports—and in February 2025, it did (restricting exports of tungsten and molybdenum products). This is another sign that the struggle for raw materials is encompassing an ever-wider list of puzzle pieces.

All these raw materials share a characteristic: they are key to technologically advanced sectors, and at the same time, their global supply is concentrated and largely tied to China. That is why warning reports have been appearing for several years (e.g., Atlantic Council 2023) about the fragility of critical mineral supply chains. Governments are beginning to act, and investors are putting capital into mining projects from Australia to Alaska. However, building an alternative ecosystem is a tedious and costly process, as we will see in Section V.

💡 KEY TAKEAWAY

Critical raw materials are the “hidden links” of technological dominance. Rare earth elements, gallium, germanium, antimony, cobalt, and tungsten—though little known to the public—determine advantages in defense and high-tech. China has monopolized many of them (e.g., 90% of REE processing, 98% of gallium, 70% of cobalt, 80% of tungsten). Therefore, it can effectively checkmate the West by restricting supply. The United States faces a huge challenge in rebuilding its own sources and supply chains for these materials to secure its national and economic security. Sections IV and V will show the implications of the current situation and how the US is trying to respond to China’s “raw material weapon.”

IV. GEOPOLITICAL AND ECONOMIC IMPLICATIONS

The conflict over critical raw materials does not occur in a vacuum—its effects radiate across a wide spectrum of issues: from the defense capabilities of nations, through the condition of strategic industrial sectors, to the stability of financial markets. In this section, we will analyze how US-China tensions over minerals translate into national security, key economic sectors, global supply chains, and markets. We will also try to understand how raw materials have become a geopolitical tool (“weaponization of supply chains”) and what this means for the global economy.

4.1 Threats to US National Security

One of the main reasons the topic of critical raw materials has hit the headlines is national security—especially American national security. The United States has realized that its dependence on China for key materials could be its Achilles’ heel in the event of a conflict. What specific threats are associated with this?

- Impact on the Defense Industrial Base: The American defense industry—from aerospace corporations (Lockheed Martin, Boeing) to ammunition manufacturers (Northrop, General Dynamics)—is inextricably linked to the supply of specialized materials. A lack of rare earth elements, antimony, titanium, tungsten, or helium-3 (another strategic isotope) could delay or even halt the production of certain weapon systems. Imagine: the F-35 cannot be built without NdFeB magnets, tank shells without tungsten, night vision devices without germanium, and ammunition without antimony. Every supply bottleneck translates into lower readiness of the armed forces. There are already reports of production delays for some missiles or satellites due to problems in obtaining special components (e.g., fiber optics for guidance systems).

- Risk of Delays and Downtime: In a military conflict scenario (e.g., a crisis over Taiwan), China would likely immediately halt the export of strategic raw materials to the US. If stockpiles have not been prepared in advance, American defense plants could face shortages after just a few days. For example, Javelin anti-tank missiles use a lot of IR components (germanium/indium compounds in the warhead)—intensive use, as seen in Ukraine, quickly depletes stocks. Replenishing them requires raw materials. Without them, the military may have the equipment, but not the ammunition.

- Vulnerability to Geopolitical Blackmail: Aware of this, the US must calculate its moves taking into account the “mineral factor.” That is, if China threatens: “don’t export weapons to Taiwan or we will cut off your rare earth supplies,” a dilemma arises. Of course, the US officially declares it will not be blackmailed, but in practice, such a threat can influence Washington’s calculations. In July 2023, when Beijing put gallium and germanium under control, Washington was in an uproar—it was interpreted as a warning: “rethink your technology sanctions, because we have our own levers.” The greater the dependence, the harder it is to pursue a tough policy towards Beijing without fear of repercussions.

- Crisis Scenarios (Atlantic Council, etc.): For a few years now, think tanks have been conducting simulations—what would happen if supplies of critical minerals suddenly disappeared? One Atlantic Council workshop (2025) considered a scenario in which China imposes a de facto ban on the export of several key minerals amid rising tensions. The conclusions were unsettling: the United States is not prepared for a prolonged interruption. Yes, it has some crisis tools—the Defense Production Act (DPA) to compel production and allocation, strategic reserves for last-resort use, and emergency purchases from allies. But these are stopgap solutions. The AC scenario assumed that the US would manage initially, but in a prolonged crisis (several months), its manufacturing capabilities would shrink drastically. In other words, stockpiles and workarounds will last for a while, but a developed economy cannot function in “besieged fortress” mode for too long. The simulation results underscored the need to accelerate diversification efforts in peacetime.

The general conclusion is that the US must treat critical raw materials as seriously as it treats, for example, nuclear readiness or cybersecurity. A lack of access to them is a new type of asymmetric threat—it’s not a missile, but it can paralyze defense capability like a thousand missiles. As a former national security advisor put it: “The enemy may not have to fire a single missile—if they cut off our supply of certain materials, they can, in a sense, disarm us slowly from within.” Of course, this applies not only to the US—other NATO countries are also vulnerable (European defense also draws on global supply chains). That is why NATO and the EU launched special initiatives in 2023 to monitor the supply of raw materials for the defense industry.

For balance, it is worth noting: China is also dependent on certain raw materials from the US and its allies—for example, grains (soybeans), some chips, and in raw materials: iron ore (Australia), nickel (Indonesia, but they have established themselves there), copper (South America), and uranium (Kazakhstan). But in the purely military sphere, China is more likely to be able to live without Western raw materials (it has invested heavily in raw material self-sufficiency). The US has a weaker starting position here.

4.2 Consequences for Key Economic Sectors

Raw material tensions do not only affect the military—they will echo through many civilian industries, from semiconductors, through automotive, to renewable energy. Let’s look at the main sectors and the consequences that restricted access to critical minerals could have for them.

Semiconductor Industry (Microelectronics):

- Threat to the AI Boom: The years 2020-2025 saw an explosion in the development of artificial intelligence, driven by increasingly powerful integrated circuits (GPUs, TPUs, specialized accelerators). These, in turn, require an extensive production and material infrastructure. The aforementioned gallium and germanium are part of this—without them, advanced sensors, 5G communication modules, or certain chip components (e.g., III-V semiconductors for RF chiplets) cannot be produced. If restrictions persist, it could slow down the development of certain AI technologies based on specialized hardware (e.g., LiDAR sensors, neuromorphic processors using memristive materials—exotic elements also appear here).

- Impact on Players like Intel, Nvidia, AMD, TSMC:

- Intel – Although it mainly produces silicon-based CPU chips, it needs equipment to build its factories (e.g., EUV lasers have components with lanthanides, precision positioning machine sensors may contain germanium, etc.). If China, for example, blocked the export of special magnets or materials for optics, the construction of new fabs could be hampered. Furthermore, Intel has 5G product lines (it once acquired Infineon Wireless), where it uses GaAs.

- Nvidia, AMD – Their GPUs are made of silicon layers, but fiber optics (Germanium) are often used for communication between chips in supercomputers, and cooling and power systems have elements containing, for example, tungsten (heat sinks, because tungsten conducts heat well and is dense). These are rather indirect dependencies, but they exist.

- TSMC, Samsung (foundries) – Like Intel, they require advanced materials for photolithography (filters made of calcium fluoride doped with rare earths?), deposition targets (some chip layers are metals like copper doped with yttrium, for example). If Chinese supplies were to run out, they would have to rely on stockpiles or more expensive sources.

- Broadcom, Skyworks, Qorvo – Producers of radio circuits. They directly need gallium arsenide and gallium nitride—and therefore gallium (China) and some indium (China ~60%). Without these raw materials, their production stops. These are key chips for smartphones and base stations, so the impact will be felt by consumer electronics giants (Apple, Huawei, etc.).

- Potential Technological Delays: If access to key materials is difficult, companies may postpone the launch of new products, waiting for stability. It may also increase R&D costs—engineers will have to design with the replacement of missing materials in mind (which is difficult and not always possible without compromises). In an extreme case—a slowdown in Moore’s Law (slower progress in chip performance). Of course, this is a worst-case scenario, as the semiconductor industry is inventive—but minor frictions could appear.

- “Chiplet” Supply Chains: Modern chips are modules produced in different places (e.g., AMD assembles its CPUs from chiplets produced at TSMC and I/O dies at GlobalFoundries). Such a chain is global—and materials fly back and forth. Raw material disruptions (e.g., tariffs, restrictions) mean more expensive transport, more bureaucracy, and even the risk of a shortage of certain elements. Koch’s Law (predicting a lengthening time-to-market for new chips) may be reinforced by geopolitical factors.

Automotive Sector:

- Electric Vehicle (EV) Production: Electric cars are rolling warehouses of critical raw materials:

- A battery of ~60 kWh contains ~8-10 kg of lithium, 20-30 kg of nickel, 5-10 kg of cobalt, and 40-50 kg of graphite. China dominates the processing of all four. If these raw materials become more expensive (which happens with restrictions) or supplies are uncertain, the cost and pace of EV production will suffer. Already in 2022, lithium prices jumped tenfold, affecting the margins of battery and car manufacturers.

- Electric motors – most EVs (except for a few, like the Tesla Model S Plaid) use neodymium magnets in their traction motors. Each such car has ~1-2 kg of NdFeB magnets (even more in hybrids). Without a supply of these magnets, heavier induction motors would have to be used, or cars would have to be put on a waiting list. In 2025, there is no Western magnet factory on the required scale (one is being built in the US, supported by the DoD).

- Electronics in cars: sensors (radars, lidars – gallium, indium, Ge), catalytic converters (cerium, lanthanum), power electronics systems (GaN in on-board chargers). Potential shortages could limit the availability of ADAS functions or charging efficiency.

- Internal Combustion Engine (ICE) Cars: Although less advanced, they also use raw materials:

- Three-way catalytic converters – platinum group metals (not China, but South Africa/Russia – also sensitive). But China does not dominate here.

- Hundreds of integrated circuits – as above, dependent on the global chip supply chain.

- Magnets in accessories (speakers, ABS sensors, small motors) – neodymium, so China.

- Overall, ICE cars are less exposed to lithium, etc., but the recent chip crisis showed how a global disruption (the pandemic) halted car production lines—decoupling could cause similar disruptions (e.g., if China stopped exporting certain electronic semi-finished products for cars due to sanctions).

- Cost Increases: Any restriction on critical raw materials -> price increase. We are already seeing the phenomenon of rising battery prices after years of decline, because raw materials have become more expensive. If this trend continues, EVs may remain more expensive than planned, delaying the price parity of EVs vs. ICE cars. This torpedoes climate and business goals (e.g., companies like Tesla have to cut margins to remain competitive).

- The “Race for Raw Materials” Option: Automakers may get involved in securing supplies themselves—for example, by signing contracts with mines in Australia, Canada, etc. This is already happening (Tesla is contracting nickel from Indonesia and New Caledonia, VW is investing in mining). This is a departure from just-in-time and the open market, and a move towards a “own your mines like in Ford’s time” model. This changes the structure of the industry and requires billion-dollar investments from automotive companies—which in the short term burdens their balance sheets, but in the long term is necessary.

Renewable Energy:

- Wind Turbines: Modern offshore (marine) wind turbines often have direct-drive generators based on neodymium magnets. Each large turbine contains hundreds of kg of Nd, Dy, Pr. In 2011, it was widely reported that one 3MW turbine contained ~2 tons of magnets. If these magnets are not available, the construction of wind farms could slow down, or it may be necessary to return to designs with gearboxes (which are less reliable). The EU and US are planning huge investments in offshore wind—but the raw materials for them are dominated by China. This is a contradiction they must resolve.

- Solar Panels: Photovoltaics is an interesting case—95% of panels are silicon cells, and here the raw material (silicon, aluminum, copper) is not the problem. The problem is that 80% of panels are made in China or with Chinese components (polycrystalline silicon, solar glass). How will decoupling change this? If the US/EU restricts imports of Chinese panels (they are already doing this with anti-dumping tariffs), they must launch their own production. In terms of raw materials, this is not difficult, but in terms of cost, it is—because China has a huge advantage of scale. Besides, thin-film panels (CdTe, CIGS) use tellurium, indium, gallium, germanium—again, raw materials controlled by a few (tellurium is a byproduct of copper, a lot of it in China).

- Energy Storage: Batteries for stationary storage are mainly lithium-iron-phosphate (LFP)—there’s no cobalt or nickel here, but there is lithium and graphite. Both—China. Alternatives like flow batteries (vanadium—most from China or Russia), sodium-ion (reassuringly, salt is everywhere, but graphite and good chemistry are needed). In any case, the energy transition planned for 2030+ rests on the availability of raw materials. The OECD warns that global climate policy could be derailed if countries fall into raw material protectionism instead of cooperating (because the common fight against climate change requires free access to panels, batteries, etc.—decoupling makes this difficult).

- Uncontrolled Costs: The years 2021-2022 already showed that the prices of raw materials like lithium and nickel can fluctuate wildly. This makes renewable energy projects financially unpredictable. Governments have to subsidize more, and companies bear the risk. This could slow down investment, as investors dislike uncertainty. The need to build local supply chains (e.g., panel factories in the US) is healthy, but more expensive (at least initially) -> less capacity will be built for the same amount of money.

In short, every transformational sector that is the backbone of the 21st-century economy will be severely affected by the rupture of global raw material supply chains. This does not mean the West will not cope—it will, but on a bumpy road, with higher costs and delays. Interestingly, China could also suffer: if the US restricts, for example, the export of advanced semiconductors, its AI development will slow down; if they block specialized materials (high-end chemistry), its industry could also come to a halt. For now, however, the asymmetry is in China’s favor for raw materials, and in the US’s favor for high-tech chips. Both, therefore, have their weak points—and both are pressing them.

4.3 Economic Weaponry and the “Weaponization” of Supply Chains

Historically, great powers have used various tools of pressure: naval blockades, financial sanctions, currency wars. In the 21st century, a new one has been added to this arsenal: manipulating the flow of critical raw materials and components. This is literally the “weaponization” of supply chains—turning them into a geopolitical weapon. China has become a master of this strategy, although the US also resorts to similar measures (e.g., chip sanctions). Let’s focus on China’s “economic raw material weapon.”

A History of Chinese Raw Material Restrictions as a Political Tool:

- We have already discussed the 2010 episode with Japan (rare earths for Senkaku).

- Another example is the embargo on the export of raw materials to Norway after the Nobel Peace Prize was awarded to a Chinese dissident (Liu Xiaobo) in 2010—China unofficially restricted, for example, the import of Norwegian salmon to exert pressure. This is not an industrial raw material, but it shows the mechanism: use a dependency (Norway was a major exporter to China) to force a political concession.

- Australia 2020: When Australia demanded an investigation into the origins of the COVID pandemic, China imposed informal sanctions on a range of Australian exports—coal, iron ore, barley, wine, beef. China hoped that hitting key industries (mining, agriculture—Australia is very dependent on the Chinese market) would force Canberra to change its tone. However, the Australians held firm (other customers helped them, e.g., India took the coal, the EU the wine, etc.), and eventually, after two years, Beijing began to lift these sanctions because it needed the raw materials (China started experiencing power shortages without Australian coal).

- South Korea 2017: After the installation of the American THAAD anti-missile system in South Korea, China targeted the Korean tourism and retail business—it banned group trips to Korea, and the Lotte Group (which had provided the land for THAAD) was practically pushed out of China (its supermarkets were closed under various pretexts). Korea felt this strongly economically, which many interpret as an expression of Chinese policy: “punish one to scare others.”

- Finally, the 2023-25 restrictions on gallium, germanium, graphite, and rare earths—these are the already described examples of the latest use of raw materials as a weapon in the dispute with the US.

In each of these cases, China chose products where the recipient was dependent on them, and China itself could do without the target market. This is important: sanctions work when they hurt one side more than the other. It’s easier for China: its huge, diversified economy can replace some sales markets or supplies, while for smaller partners, losing access to China can be painful (e.g., for Australia, a third of whose exports went to China). In the case of the US, China knows its raw materials are critical, and it can, for example, redirect exports to others (gallium and germanium can go to Europe or into storage instead of the US, to drive up prices).

The “Market Flooding” Strategy – Price Manipulation:

- An interesting tactic is not only cutting off supplies but, on the contrary, flooding the market with a given raw material to control the price and make competitors dependent. China has used this for years:

- In the 1990s, it flooded the market with cheap rare earths—prices fell by ~95%, Mountain Pass couldn’t withstand it and collapsed. When it became a monopoly, it later briefly tightened exports (which caused prices to soar in 2010).

- Lithium in 2018–2019: After the 2016-17 boom (lithium prices went up, many Western companies started planning mining projects), a supply glut occurred in 2018—largely coordinated by Chinese companies in Australia (Greenbushes increased production) and South America (deals with Chile). Lithium prices fell from $20k to $7k per ton. The effect: many Western lithium projects became unprofitable and were frozen. Then, China bought up assets cheaply or eliminated its competition. (By 2021, demand picked up and prices jumped again, but in the meantime, China’s dominance in refining had solidified).

- Nickel in 2021–22: Here, there was the famous short squeeze (not initiated by China, but by a Chinese fund that got ahead of itself). China’s Tsingshan assumed nickel prices would fall because it had overinvested in Indonesia and was flooding the market with NPI nickel, and it shorted contracts—a miscalculation caused a price spike and a crash on the LME. The details are less important—suffice it to say that by producing cheap NPI nickel, China made it so that, for example, the Talon Metals project in the US (sponsored by Tesla) is still economically uncertain. Because when nickel prices are artificially low, new mines won’t start.

- Antimony: As already mentioned, after the announcement of support for the Stibnite mine, Chinese media suggested that China could easily increase antimony production and bring down the price to make the Perpetua project unprofitable. In the end, it’s a race: will the US start its mine before China possibly buries the project by flooding the market? The problem is that antimony is such a small market (in terms of value) that China can manipulate it almost cost-free.